Understanding the Difference, Pros & Cons for Smarter Money Management

🧩 Overview

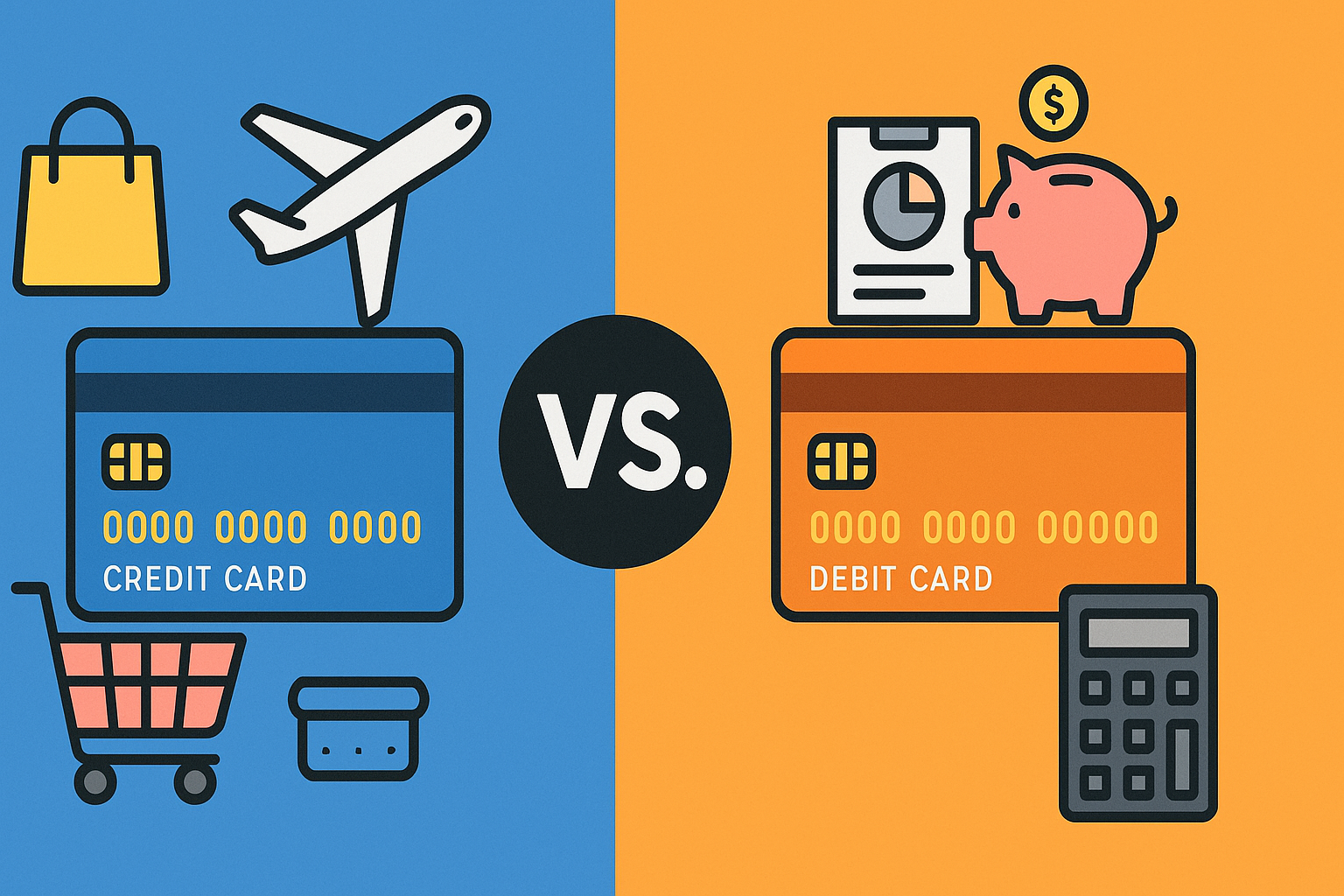

Credit Card vs Debit Card — this has become one of the most common financial comparisons in India today. In our increasingly digital world, almost every Indian carries one or both cards. But the question remains: which is better for you?

In today’s digital world, almost every Indian carries either a credit card or a debit card, and many people own both. Yet, one key question remains:

Which is better — a credit card or a debit card?

While both cards look the same, their purpose and functioning are very different.

A credit card allows you to borrow money from the bank and pay it back later, while a debit card directly deducts funds from your bank account.

Choosing the right one impacts your spending habits, savings, and even your credit score.

Let’s break down the major differences, pros, and cons to help you decide which one fits your lifestyle in 2025.

When I first started managing my expenses, I only used a debit card because it felt safer — I could literally see my balance drop after every purchase. But once I got my first credit card, I realized how much difference it makes when used smartly — especially for cashback and travel offers

💠 What Is a Credit Card?

A credit card lets you borrow funds from the bank up to a fixed credit limit. You can spend now and repay later, usually within a 30–45 day interest-free period.

🔹 Key Features

- Borrow money within your credit limit

- Earn cashback, reward points, and travel miles

- Build or improve your CIBIL score

- Convert large purchases into EMIs

- Accepted globally — online and offline

- Get purchase protection and travel insurance

✅ Example

If you buy a ₹10,000 phone using your credit card, you can repay it next month or convert it into a 6-month EMI.

💳 What Is a Debit Card?

A debit card is directly linked to your savings or current account. When you make a transaction, the amount is instantly deducted — so you only spend what you have.

🔹 Key Features

- Immediate payment from your bank account

- No interest or late payment charges

- Easy cash withdrawal at ATMs

- Great for budget control and beginners

- Issued automatically with most bank accounts

✅ Example

If you use your debit card for ₹2,000 groceries, the money leaves your account instantly — no future bills or interest.

⚖️ Credit Card vs Debit Card – Quick Comparison Table

| Feature | Credit Card | Debit Card |

|---|---|---|

| Source of Funds | Borrowed from Bank | Directly from Account |

| Interest | Charged if unpaid | None |

| Credit Score Impact | Builds CIBIL Score | No impact |

| Rewards | Cashback, Points, Miles | Limited rewards |

| EMI Facility | Yes | No |

| Risk of Overspending | High | Low |

| Ideal For | Travel, Emergencies, Large Purchases | Daily Expenses, Beginners |

🌟 Benefits of Using a Credit Card

- Builds Credit History – Improves your CIBIL score with responsible use

- Exclusive Rewards – Cashback, discounts, and travel perks

- Emergency Backup – Helps when you’re short on cash

- EMI Option – Split big payments over months

- Free Insurance – Fraud, travel, and purchase protection

⚠️ Disadvantages

- High interest (up to 36% annually)

- Late payment penalties

- Easy to fall into debt if used carelessly

For example, last year I booked my flight tickets with a credit card and got ₹1,200 cashback plus free lounge access. If I had used my debit card, I would’ve paid the full price without any rewards.

That’s when I understood — a credit card isn’t just for spending, it can actually save money if used wisely.

💰 Benefits of Using a Debit Card

- Spend only what you have — no debt risk

- No interest or late fees

- Instant payments for groceries, fuel, or bills

- Easy ATM access

- Great for students and beginners

⚠️ Limitations

- No impact on credit score

- Limited rewards

- Not ideal for emergencies or large travel bookings

🔒 Which Is Safer to Use?

Both cards are safe if used wisely, but credit cards offer stronger fraud protection.

If your credit card is misused online, the bank usually reverses the charges quickly.

However, with a debit card, the money is deducted instantly, and recovery can take longer.

👉 For online shopping and travel bookings, credit cards are the safer option.

📅 When to Use Each Card

Use a Credit Card for:

- Online shopping (for offers and cashback)

- Flight or hotel bookings

- Emergency or large purchases

- Earning rewards and building credit

Use a Debit Card for:

- Groceries, fuel, and everyday spending

- ATM withdrawals

- Budget tracking

- Beginners learning money discipline

💡 Expert Tips for Using Both Wisely

- Always pay your credit card bill on time to avoid interest

- Keep credit utilization below 30%

- Use your debit card for routine expenses

- Regularly check your statements for fraud or errors

- Avoid cash withdrawals using credit cards

🧠 FAQs – Credit Card vs Debit Card in 2025

Q1. Which is better: Credit Card or Debit Card?

Both are useful. Credit cards are best for rewards and emergencies; debit cards are safer for budgeting.

Q2. Does using a debit card build your CIBIL score?

No. Debit cards don’t affect your credit score.

Q3. Are credit cards safe for online transactions?

Yes. Credit cards have stronger fraud protection and chargeback rights.

Q4. Which is better for students?

A debit card is ideal for beginners. Later, a student credit card can help build credit history.

Q5. Can I use both cards together?

Yes! Use debit cards for daily needs and credit cards for big or reward-eligible purchases.

🏁 Conclusion

There’s no clear winner in the credit card vs debit card debate — both serve different purposes.

A credit card offers flexibility, rewards, and credit-building potential, while a debit card ensures spending discipline and simplicity.

👉 Smart users use both together — debit for everyday expenses, credit for rewards and emergencies. That’s the key to balanced financial health in 2025.

Personally, I don’t think it’s about choosing one over the other. I keep both in my wallet — debit for daily use, credit for travel or emergencies. This balance keeps my spending under control and also helps me maintain a healthy credit score.

Fantastic website. Lots of helpful information here. I’m sending it to several buddies ans also sharing in delicious. And certainly, thanks on your sweat!